(著)山たー

MatlabやRでは線形回帰のモデルをfitして以下のように結果を表示してくれるライブラリがある。

R

> sample=read.csv("boston_housing_data.csv")

> model=lm(Y~., data=sample)

> summary(model)

Call:

lm(formula = Y ~ ., data = sample)

Residuals:

Min 1Q Median 3Q Max

-15.5795 -2.7256 -0.5165 1.7831 26.1887

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.649e+01 5.104e+00 7.149 3.18e-12 ***

CRIM -1.072e-01 3.271e-02 -3.276 0.001126 **

ZN 4.640e-02 1.373e-02 3.380 0.000784 ***

INDUS 2.086e-02 6.150e-02 0.339 0.734597

CHAS 2.689e+00 8.616e-01 3.120 0.001912 **

NOX -1.780e+01 3.821e+00 -4.658 4.12e-06 ***

RM 3.805e+00 4.180e-01 9.102 < 2e-16 ***

AGE 7.511e-04 1.321e-02 0.057 0.954686

DIS -1.476e+00 1.995e-01 -7.398 6.02e-13 ***

RAD 3.057e-01 6.633e-02 4.608 5.19e-06 ***

TAX -1.233e-02 3.761e-03 -3.278 0.001118 **

PTRATIO -9.535e-01 1.308e-01 -7.287 1.27e-12 ***

B 9.392e-03 2.684e-03 3.500 0.000507 ***

LSTAT -5.255e-01 5.069e-02 -10.366 < 2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 4.746 on 492 degrees of freedom

Multiple R-squared: 0.7406, Adjusted R-squared: 0.7338

F-statistic: 108.1 on 13 and 492 DF, p-value: < 2.2e-16

Matlab

mdl =

線形回帰モデル:

y ~ 1 + x1 + x2 + x3 + x4 + x5 + x6 + x7 + x8 + x9 + x10 + x11 + x12 + x13

推定された係数:

Estimate SE tStat pValue

__________ _________ ________ __________

(Intercept) 36.491 5.1045 7.1488 3.1824e-12

x1 -0.10717 0.032712 -3.2762 0.0011264

x2 0.046395 0.013728 3.3796 0.00078361

x3 0.02086 0.061497 0.33921 0.7346

x4 2.6886 0.86162 3.1204 0.0019123

x5 -17.796 3.8206 -4.6579 4.1173e-06

x6 3.8048 0.418 9.1023 2.2075e-18

x7 0.00075106 0.013211 0.056852 0.95469

x8 -1.4758 0.19948 -7.3979 6.0177e-13

x9 0.30566 0.066333 4.6079 5.1897e-06

x10 -0.012329 0.0037608 -3.2784 0.0011178

x11 -0.95346 0.13084 -7.2872 1.2682e-12

x12 0.0093925 0.0026835 3.5001 0.00050729

x13 -0.52547 0.05069 -10.366 6.5958e-23

観測数: 506、誤差の自由度: 492

平方根平均二乗誤差: 4.75

決定係数: 0.741、自由度調整済み決定係数 0.734

F 統計量と一定のモデルの比較: 108、p 値は 6.95e-135 です

これを表示するプログラムをPythonで書いてみる。

ソースコード

import numpy as np

import pandas as pd

from sklearn.datasets import load_boston

import scipy as sp

#データを計画行列に変換

def make_design_matrix(X,n):

return np.concatenate([np.ones((n,1)), X], axis=1)

#正規方程式を解いて係数の推定値を計算

def estimate(X,y):

return np.linalg.inv(X.T @ X) @ X.T @ y

#残差を計算

def residual_error(X,y):

residual = y - estimate(X,y) @ X.T

return residual

#標準誤差(standard error)

def St_Error(X,y,n,p):

#残差を計算

residual=residual_error(X,y)

#残差平方和Sを計算

S=np.sum(residual.T @ residual)

#推定値の分散を計算

var_estimate=(1/(n-p-1))*S*np.linalg.inv(X.T @ X)

#対角成分を取って平方根を取る

StdE=np.sqrt(np.diag(var_estimate))

return StdE

#t値

def t_value(estimate, StdE):

return estimate/StdE

#p値

def p_value(t,n,p):

return 2*(1-sp.stats.t.cdf(np.abs(t),n-p-1))

#線形回帰

def linearMod(X,y,n,p):

Xd=make_design_matrix(X,n)

beta=estimate(Xd,y)

StdE=St_Error(Xd,y,n,p)

tValue=t_value(beta,StdE)

pValue=p_value(tValue,n,p)

matrix=np.concatenate([beta, StdE,tValue,pValue], axis=0)

matrix=np.reshape(matrix,(4,p+1)).T

indexlist=['(Intercept)']

indexlist.extend(['x'+str(i) for i in range(1,p+1)])

df=pd.DataFrame(matrix,

index=indexlist,

columns=('Estimate', 'Std. Error','t value','Pr(>|t|)'))

return df

#Boston Housing Dataをインポート

boston = load_boston()

X=boston.data

y=boston.target

n=X.shape[0] #サンプル数

p=X.shape[1] #説明変数の数

#線形モデルにfit

model=linearMod(X,y,n,p)

#結果表示

print('Coefficients:')

print(model)

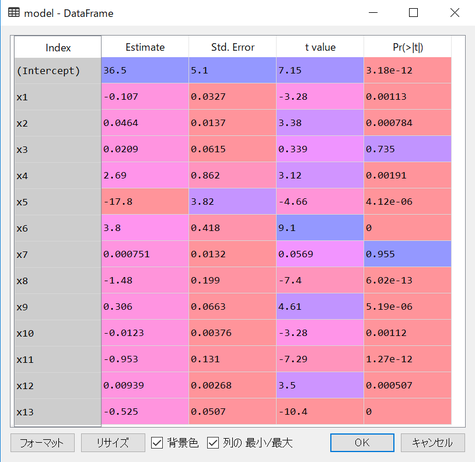

結果

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 36.491103 5.104500 7.148811 3.182565e-12

x1 -0.107171 0.032712 -3.276202 1.126402e-03

x2 0.046395 0.013728 3.379596 7.836070e-04

x3 0.020860 0.061497 0.339209 7.345971e-01

x4 2.688561 0.861617 3.120369 1.912339e-03

x5 -17.795759 3.820585 -4.657862 4.117296e-06

x6 3.804752 0.417998 9.102313 0.000000e+00

x7 0.000751 0.013211 0.056852 9.546859e-01

x8 -1.475759 0.199483 -7.397902 6.017409e-13

x9 0.305655 0.066333 4.607863 5.189664e-06

x10 -0.012329 0.003761 -3.278408 1.117826e-03

x11 -0.953464 0.130841 -7.287219 1.268097e-12

x12 0.009393 0.002683 3.500142 5.072875e-04

x13 -0.525467 0.050690 -10.366343 0.000000e+00

他の部分は次の機会につくる。

コメントをお書きください